Table of Contents

ToggleWhat is a Credit Score?

A credit score is your report card for how you handle money. It’s a number, ranging from 300 to 900, that informs lenders whether you’re likely to repay a loan on schedule. The higher your score, the more likely you are to qualify for credit and at lower interest rates.

Credit scores are determined by factors such as:

Your payment history

The proportion of credit you’ve utilized

The number of credit cards or loans you hold

Your previous defaults or arrears

If you’ve previously borrowed responsibly, you’ll likely have a positive credit score. If you’ve never borrowed, you may not even have a score.

Why Is a Credit Score Important?

Lenders use credit scores to make rapid judgments on:

Who to borrow from

How much to borrow

What rate of interest to charge

A good credit rating makes it easy for you to obtain credit. A bad or non-existent score makes it difficult to borrow or leads to a higher rate. For decades, this system served borrowers who had stable, salaried employment and a borrowing record.

But in 2025, that no longer suffices.

The Problem with Traditional Credit Scoring

1. The Credit-Invisible Majority

Millions of people in India—gig workers, freelancers, first-time borrowers—don’t have a formal credit history. That doesn’t mean they’re risky. It just means they’ve never used credit before.

Old credit scoring models don’t know what to do with them. No credit history means no score. No score means no access to loans. This cycle of invisibility is now being challenged by lenders who want to serve this growing segment.

2. Work Has Changed. So Should Risk Models.

Today’s workforce looks very different from even a decade ago. People no longer stick to the same job for years. Many earn through gig platforms, freelance projects, or remote work. But traditional credit models don’t capture this.

A delivery head earning consistently on platforms or a content person with recurring brand partnerships might not have a salary voucher, but he does possess steady income. The lenders are now looking towards alternate data—such as bank statements, UPI transactions, rent payments, and utility bills—to gain insights into these borrowers.

3. Real-Time Credit Needs Real-Time Data

The credit landscape today is quick. Whether instant loans, embedded credit at checkout, or Buy Now, Pay Later (BNPL), in all cases, decisions have to be made within seconds.

Credit scores, however, reflect historic behavior, not activity in real-time. Lenders now need to know:

Is the individual currently employed?

Are they actively drawing on their bank account?

Do they have active debts?

Software such as payroll APIs, bank statement analysis, and real-time KYC checks assist in answering these questions in real time, resulting in quicker, wiser loan decisions.

The Emergence of Embedded Lending

Embedded finance equates to lending at the moment of need, during shopping, travel bookings, or insurance premium payments.

But here’s the catch: lenders no longer own the entire customer experience. They only get a few seconds to make a call. Ancient credit systems won’t operate within that time frame.

Instead, they are relying on API-powered tools such as:

Instant PAN and Aadhaar checks

Mobile-linked credit scores

Bank account ownership verification

These are lightweight, instant, and integrated into digital experiences—taking trust and risk verifications into every transaction.

Regulators Are Opening the Gates

Lenders are not alone in looking ahead. Regulators are also promoting a more expansive creditworthiness perspective.

India’s Account Aggregator (AA) system enables customers to securely share their financial information and with complete agreement. This translates into lenders having access to more applicable, timely data in order to assess borrowers.

Digital public infrastructure such as Aadhaar, DigiLocker, and UPI also leaves a robust identity and transaction history that can be used to authenticate the financial credibility of an individual.

In summary, regulators are encouraging a more equitable credit system.

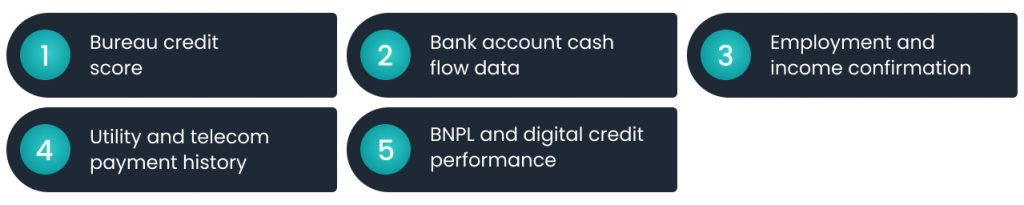

Hybrid Scoring Models: A Wiser Strategy

Nobody’s saying the old-fashioned credit score is obsolete. It still has a place. But in 2025, the most savvy lenders are using multiple data points to get the whole picture.

A hybrid scoring model can include:

Bank account cash flow data

Employment and income confirmation

Utility and telecom payment history

BNPL and digital credit performance

This enables lenders to provide more nuanced financial products. For example, a Mumbai salaried worker and Rajasthan dairy farmer can both borrow—but with very different data inputs.

Redefining Creditworthiness Is a Competitive Advantage

Those lenders who evolve with new credit models can benefit significantly. With access to more comprehensive and up-to-date data, they are able to:

Reach new segments of borrowers

Lower default rates

Enhance unit economics

Strengthen customer relationships

They’re not just providing more loans—better, safer, and smarter loans.

Final Thoughts

In 2025, creditworthiness is no longer merely a reflection of your history. It’s a reflection of your present behavior, spending habits, and online activity.

Credit scores continue to exist, but the philosophy behind them is changing. Lenders who get this will not only grow faster, but they’ll also chart the course of financial inclusion.

Frequently Asked Questions (FAQs)

Q. What is a credit score?

A credit score is a number indicating how probable you are to repay borrowed funds depending on your past behavior regarding money.

Q. Why is my credit score significant?

It assists banks and lenders in determining whether to accept your loan or credit card application and at what interest rate.

Q. Do I need a credit score to have a loan?

Yes. Increasingly, lenders are employing alternative data such as bank activity, bill payments, and employment verification to gauge new borrowers.

Q. What is alternative credit data?

Alternative data comprise data such as UPI transactions, rent payments, utility bills, and gig income, utilized to determine your creditworthiness when conventional data is not available.

Leave a Reply