Table of Contents

ToggleAs companies grow and expand their digital landscapes, their reliance on outside partners – vendors, suppliers, agents, and contractors—has escalated many fold. So too has their risk.

In 2025, your greatest security or compliance violation might not be from within—perhaps it will originate from an unvetted third-party partner.

Read More: Securing Vendor Partnerships

What Is Third-Party Due Diligence?

Third-party due diligence (TPDD) is a systematic exercise in evaluating, validating, and tracking outside parties with which the company transacts business, be it supply chain, lending, franchisee, or services delivery.

It provides answers to queries such as:

Is the third party compliant with the law?

Do they have undisclosed litigation or financial warning signs?

Are they trustworthy enough to entrust your money, information, or reputation to?

Are they genuine, registered, and in business?

When executed correctly, TPDD enhances resilience, improves compliance, and fosters long-term business relationships.

Speed vs. Risk Conundrum

Digital-native organizations, particularly fintech, e-commerce, healthcare, and logistics firms, commonly onboard hundreds of suppliers every month. However, such velocity creates blind spots:

Inconsistent or manual verification

Paperwork-induced onboarding delays

Too much reliance on human discretion

Risk of fraud, shell companies, and compliance failures

As per ItPro, 62% of companies experienced a data breach in 2023 because of weaknesses in third-party software supply chains.

A Contemporary TPDD Framework Addresses 6 Risk Layers

Successful due diligence in 2025 must address multiple dimensions. Here’s how thorough TPDD appears:

1. Operational Risk

Business and operational nature

Reach and locality

Verification of premises

2. Management Risk

Director profiles

Fraud or litigations history

Sanctions and worldwide watchlists

3. Financial Health

GST filings, verification of bank accounts

MCA ratios, shareholding trends

Insolvency or default history

4. Legal & Reputational Risk

Civil or criminal case records

Negative media hits

Brand damage potential

5. Compliance Risk

PAN, GSTIN, Udyam, PF, ESIC checks

Regulatory adherence

Sectoral compliance frameworks

6. Physical Site Verification

GPS-tagged field checks

Photographic evidence

Agent feedback and validation

This 360-degree model prevents future risks—whether financial, legal, or reputational.

Data Points That Shouldn’t Be Ignored

A 2024 EY report points out some disturbing facts:

49% of organizations don’t have uniform third-party monitoring practices

80% of them had a third-party-related incident

Global enforcement action for third-party-related fraud increased 34% year-over-year

How OnGrid Powers Intelligent TPDD at Scale

OnGrid provides a digital-first, API-based TPDD platform designed to manage sophisticated and high-volume onboarding cases.

Key Features:

PAN, GSTIN, Udyam, CIN, Shop Act verifications

MCA deep-dives (financials, shareholding, directors)

Sanctions, PEP, and litigation screening

Adverse media and reputation tracking

KYC / KYB checks with government databases

Field verification with GPS, photos, and agent inputs

Batch imports and real-time integrations through secure APIs

OnGrid’s platform is SOC 2 Type II, ISO 27001, and ISO 27701 certified to ensure complete data security, privacy, and audit readiness.

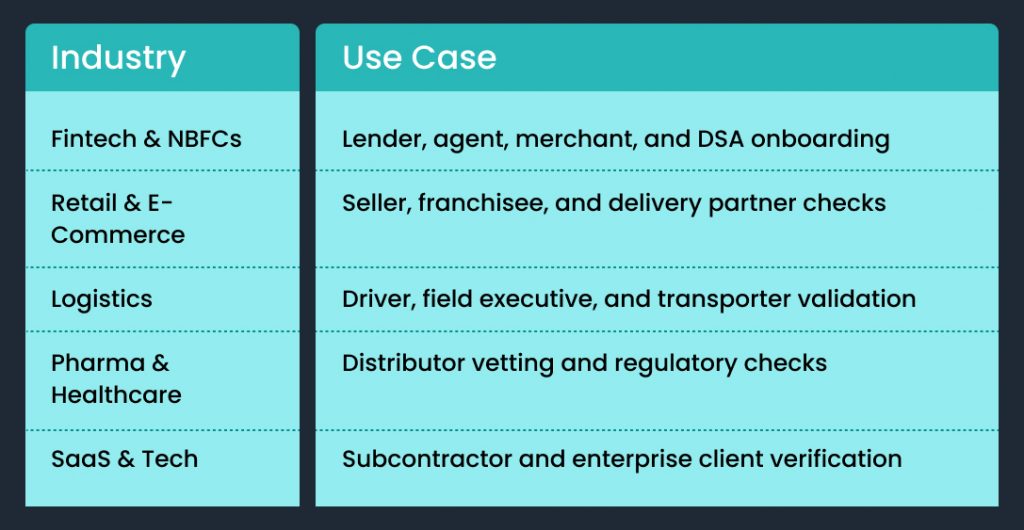

Where It Applies: Industry Use Cases

Why Due Diligence Must Be Ongoing, Not Singular

Regulatory, financial, and operating environments evolve continuously. It is no longer sufficient to depend on a single check.

Directors step down or are removed

Firms change operations or names

Financial stability can shift quarterly

Regulatory regulations change

Monitoring in real-time is the future of third-party risk management.

FAQs: All You Want to Know About TPDD

Q1: Who should conduct third-party due diligence?

Any company dealing with vendors, suppliers, franchisees, financial agents, or logistics partners, particularly in regulated industries such as finance, pharma, insurance, and lending.

Q2: How is TPDD distinct from KYC or KYB?

KYC/KYB is identity-level vetting. TPDD is more comprehensive—verifying operations, legal status, finances, physical presence, and reputation.

Q3: How frequently should third-party checks be conducted?

TPDD must be conducted at onboarding and reassessed from time to time (every 6-12 months) based on the risk profile.

Q4: Is TPDD mandatory in India?

Yes, TPDD is more and more mentioned in:

RBI KYC Master Direction for NBFCs and Banks

Prevention of Money Laundering Act (PMLA)

DPDP Act, 2023

SEBI and IRDAI guidelines for intermediaries

Failure to exercise due diligence can lead to severe fines and reputational loss.

Q5: Can startups leverage TPDD?

Absolutely. Even small firms require the guarantees that suppliers or technology partners are not exposing them to undisclosed risk—particularly when growing quickly or handling sensitive information.

Want to see TPDD in action? Schedule your walkthrough today.

Sources:

Leave a Reply